The Austin housing market has always had a rhythm of its own. From rapid appreciation to periods of normalization, buyers here have learned that timing isn’t everything—strategy is.

Today, with borrowing costs higher than what many grew used to over the past few years, affordability has become the central conversation at every kitchen table and showing.

But here’s the thing: seasoned buyers and savvy agents know that higher rates don’t mean you have to sit on the sidelines. It simply means you need to get more creative with how you structure your deal.

That’s where financing tools—often overlooked—can make a meaningful difference in your monthly budget and long-term financial comfort.

One of the most powerful tools available right now is Austin mortgage rate buydowns, a strategy that allows buyers to step into homeownership with reduced payments upfront while keeping their long-term options open.

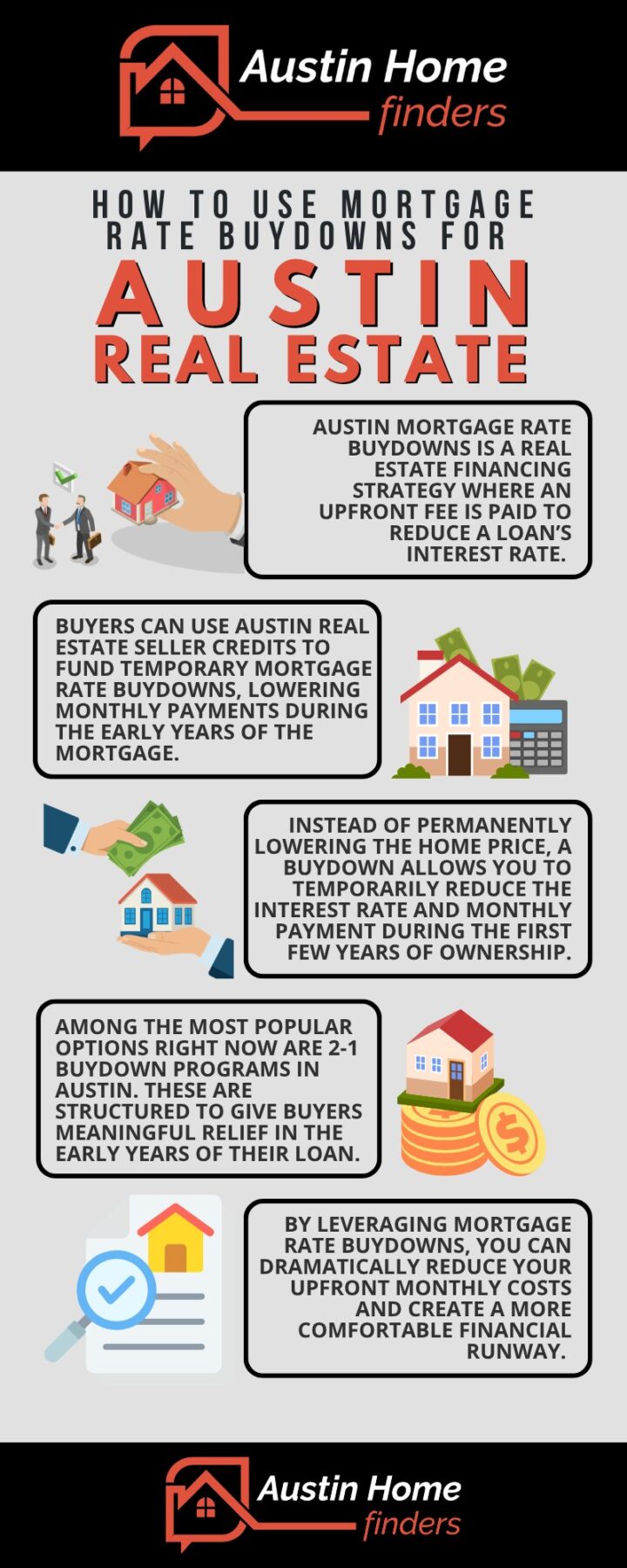

What Are Austin Mortgage Rate Buydowns

Austin mortgage rate buydowns are financing strategies where an upfront fee is paid to reduce a loan’s interest rate. Buyers often use Austin real estate seller credits to fund temporary mortgage rate buydowns in Texas, lowering monthly payments during the early years of the mortgage and easing the transition into homeownership.

Navigating High Austin Mortgage Rates

The Affordability Challenge

There’s no way around it—Austin mortgage rates today are higher than what many buyers were accustomed to just a few years ago. And that shift has had a direct impact on purchasing power.

Even a 1% increase in interest rates can significantly raise your monthly payment, sometimes by hundreds of dollars. For many buyers, that means adjusting expectations—whether it’s the size of the home, the neighborhood, or the overall budget.

This is exactly why strategic financing has become so critical. Instead of stretching your budget or delaying your purchase, buyers are now exploring ways to reduce their initial monthly obligations at closing.

The Buydown Solution

This is where buydowns shine. Rather than permanently lowering the price of a home, a buydown allows you to temporarily reduce your interest rate—and therefore your monthly payment—during the first few years of ownership.

Think of it as a financial cushion. It gives you time to grow into your mortgage. Maybe your income is expected to rise. Maybe you’re planning to refinance when rates stabilize. Either way, buydowns create breathing room when you need it most.

Leveraging 2-1 Buydown Programs in Austin

How the Numbers Work

Among the most popular options right now are 2-1 buydown programs in Austin. These are structured to give buyers meaningful relief in the early years of their loan.

Here’s how it works:

- Year 1: Your interest rate is reduced by 2%

- Year 2: Your rate is reduced by 1%

- Year 3 onward: The loan returns to the full, fixed note rate

Let’s say your locked rate is 6.5%. With a 2-1 buydown, you’d pay as if your rate were 4.5% in year one and 5.5% in year two before settling into the full rate.

That difference can translate into substantial monthly savings—often enough to make a home comfortably affordable rather than financially stressful.

Qualifying for the Loan

Here’s an important detail many buyers overlook: lenders will still qualify you based on the full note rate, not the reduced rate during the buydown period.

Why? Because they want to ensure you can comfortably afford the mortgage once the temporary reductions expire.

This is actually a good safeguard. It prevents buyers from overextending themselves and ensures that when the loan resets to its standard rate, there are no surprises.

Negotiating Seller-Paid Interest Rate Buy Downs in Austin

The Negotiation Strategy

In today’s real estate market, negotiation has evolved. Instead of simply asking for a price reduction, many buyers are requesting Austin real estate seller credits to fund their buydown.

Why does this matter? Because a seller contributing toward a buydown can often provide more real financial benefit to the buyer than a small reduction in price. A lower monthly payment impacts your day-to-day life far more than a slightly lower purchase price.

This is where seller-paid interest rate buy downs Austin become a powerful tool.

A Win-Win for Both Parties

From the seller’s perspective, offering a credit toward a buydown allows them to maintain their asking price—protecting the perceived value of their home and supporting neighborhood comps.

From the buyer’s perspective, it’s a game changer. You walk into your new home with significantly reduced payments during the most financially sensitive period of ownership. It’s one of those rare scenarios in real estate where both sides genuinely benefit.

Buydown Strategy Comparison Table

Here’s a quick breakdown to help you compare your options:

| Buydown Type | Rate Reduction Structure | Typical Duration | Best Use Case |

|---|---|---|---|

| 2-1 Buydown | 2% Year 1, 1% Year 2 | 2 Years | Expecting future income increases |

| 3-2-1 Buydown | 3% Year 1, 2% Year 2, 1% Year 3 | 3 Years | Seeking maximum initial relief |

| 1-0 Buydown | 1% Year 1 | 1 Year | Short-term payment adjustment |

| Permanent Buydown | Fixed reduction (e.g., 0.25%) | Life of Loan | Long-term homeowners seeking stability |

Each strategy serves a different goal, so the right choice depends on your financial outlook, timeline, and comfort with future market conditions.

Key Takeaway

Navigating today’s Austin mortgage rates doesn’t have to mean compromising your goals or delaying your move. With the right approach, you can structure a deal that works in your favor from day one.

By leveraging Austin mortgage rate buydowns and negotiating seller-paid interest rate buy downs Austin through Austin real estate seller credits, you can dramatically reduce your upfront monthly costs and create a more comfortable financial runway.

In a market that rewards strategy, this is one of the smartest ways to secure a home while maintaining flexibility for the future.

If you’re considering buying in Austin and want to explore how these strategies can work for your specific situation, it’s worth having a conversation with someone who understands how to structure these deals effectively.

Reach out today at 512-779-6745 or email joeschleis@realtyaustin.com to get personalized guidance and start building a smarter path to homeownership.

Frequently Asked Questions

How much do Austin real estate seller credits typically need to be to fund a 2-1 buydown?

It varies, but typically ranges from 1% to 2.5% of the loan amount, depending on the rate and lender structure.

Are temporary mortgage rate buydowns in Texas available for investment properties?

Generally, they are more common for primary residences and second homes, but some lenders do offer options for investment properties.

What happens to the unused buydown funds if I refinance my Austin home after one year?

Any unused funds are typically applied toward your loan principal.

Can I use my own money to fund Austin mortgage rate buydowns instead of the seller?

Yes, buyers can absolutely fund the buydown themselves if seller credits are not negotiated.

How do Austin mortgage rates today compare to the rates offered through a 3-2-1 buydown?

A 3-2-1 buydown significantly reduces your effective rate in the early years, sometimes by as much as 3% in year one.

Do 2-1 buydown programs in Austin apply to both FHA and Conventional loans?

Yes, many lenders offer buydown options for both loan types, though guidelines may vary.

Why might a seller prefer to offer seller-paid interest rate buy-downs in Austin rather than a price cut?

Because it preserves the home’s sale price while still making the deal more attractive to buyers.